By Ryan Stueber

While it is usually quite straightforward to get an Earthquake Insurance policy, understanding how the policy works and the options you can choose from is not. If you’re more interested in the answer to “Should I have earthquake insurance?“, take a look at that article and then come back to this one. In this article we will break down the different parts of an Earthquake Policy in detail so you understand your options as well as how the coverage applies in a real life scenario.

Different Types of Earthquake Insurance Coverage

Earthquake Insurance policies do vary quite a bit from company to company but there are two primary coverage forms that most companies adhere to.

- Standard Coverage

- Comprehensive Coverage

Covers only the home itself in the event of an earthquake.

Covers the home, your belongings, and pays for you to live somewhere else while you home is being repaired or rebuilt.

Because the cost difference is not huge, most clients opt for the comprehensive option for their primary home and the standard coverage for any secondary homes or rental properties they own.

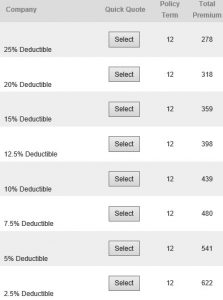

Your Earthquake Insurance Deductible

Deductibles on Earthquake Insurance are generally based on a percentage of total coverage and can range between 2.5% and 25%. As you might imagine, the lower the deductible, the higher the cost. The illustration below shows the range of premiums and deductibles base on $303,000 in dwelling coverage on a home in Tacoma.

Once you choose a deductible, it’s important to understand how it works.

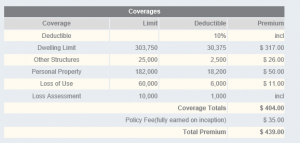

Let’s say you chose a 10% deductible for the aforementioned house in Tacoma.

Here is the proposal.

Based on this illustration you can see exactly what that 10% deductible works out to for each coverage. But remember, the deductible is based on the total coverage amount in each row, not the cost of the damage.

If we had an earthquake and your home was damaged along with your personal property and you couldn’t live in the home while the repairs were being done, your total deductible would actually be $30,375 +$18,200 +$6000 = $54,575.

But wait a minute you say! I have to come up with $54,575 before the insurance company will pay any damages? Thankfully, Earthquake Insurance deductibles work differently than a typical Home Insurance deductible. The Earthquake Insurance company will pay out everything up to your deductible rather than collecting it up front. So let’s say there was $200,000 in damage to your house. They would pay out $169,625 for the repairs and the leave the remaining $30,375 for you to pay at the end.

Why do Earthquake Insurance policies have such high deductibles?

Companies that offer Earthquake Insurance are taking on a lot of risk for a relatively low amount of premium. This means that they can’t afford to pay out claims on every 3.5 magnitude earthquake that causes a few cracks in your drywall. The deductible is designed specifically to prevent the filing of small claims caused by lesser earthquakes. That allows the insurance company to save their premium dollars for the big damage caused by a large earthquake and make their policies cost effective for more people.

What If I can’t rebuild in the same location or don’t want to after an earthquake?

One of the best features of most Earthquake Insurance policies is that they allow you to rebuild elsewhere if the home is a total loss and it’s just not safe to rebuild in that location. You can use the insurance money to pay off your existing mortgage and move to another area if you would like to. If you own your home free and clear, you can use the money to build a new home in a location of your choosing.

Hopefully you’ve found this a helpful guide and please feel free to reach out to us with further questions or to request a quote!