As temperatures drop and we all start prepping for the chilly season ahead, homeowners often ask:

“What can I do to help prepare my home for winter?”

Here are a few high-impact upgrades that not only help your home run more efficiently but also reduce your risk for costly winter claims.

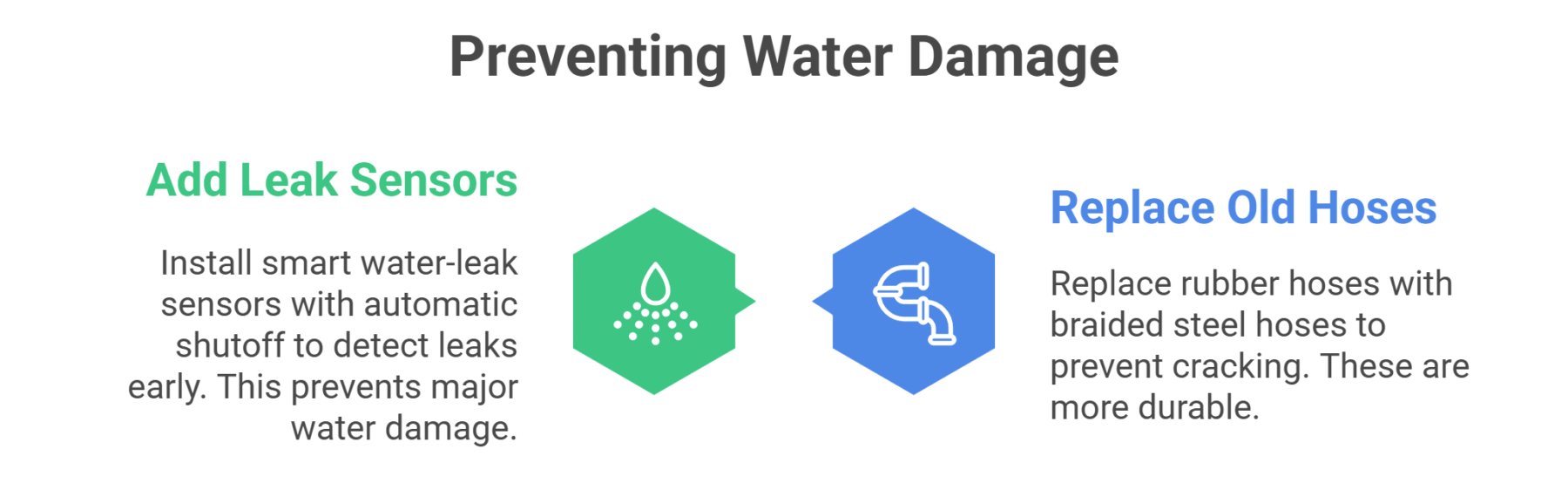

Stop Water Damage Before It Starts

Frozen or burst pipes are one of the most common (and expensive) winter claims. A few simple upgrades can save you a lot of headaches later:

- Replace old supply hoses on your washing machine, dishwasher, and fridge with braided steel ones. They’re less likely to crack or burst.

- Add smart water-leak sensors with automatic shutoff. These systems detect leaks early and prevent major water damage. Many insurers even offer credits for protective devices like these. You may qualify for a protective-device credit where available.

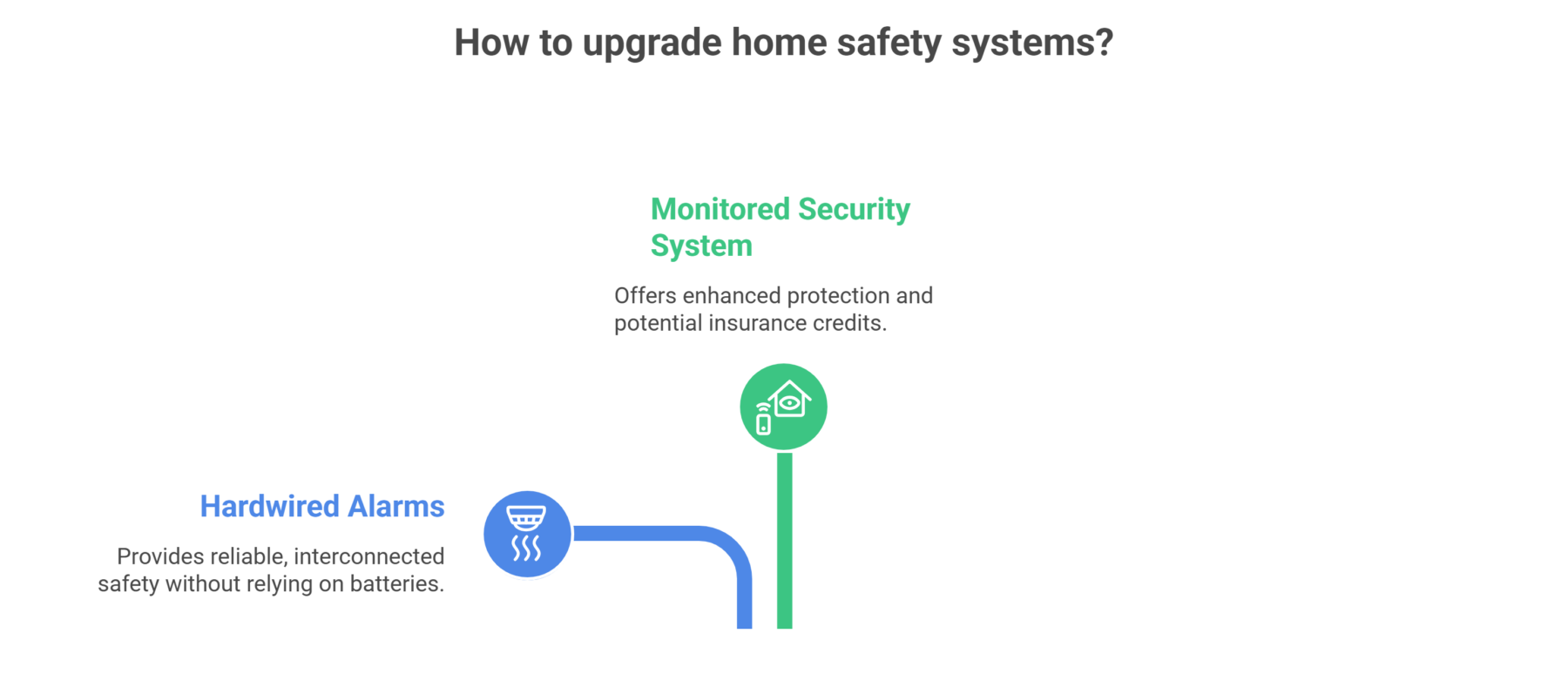

Upgrade Smoke, CO, and Security Systems

If your smoke or carbon monoxide alarms are battery-operated or outdated, now’s the time to switch to hardwired, interconnected alarms.

Better yet, connect them to a monitored security system. It adds an extra layer of protection and may qualify for a protective-device credit where available.

Schedule Furnace/Heat Pump Maintenance

Before winter hits full swing, schedule a professional tune-up for your furnace, heat pump or home heating system. Regular maintenance helps prevent breakdowns, reduces fire risk, and ensures your heating system runs efficiently.

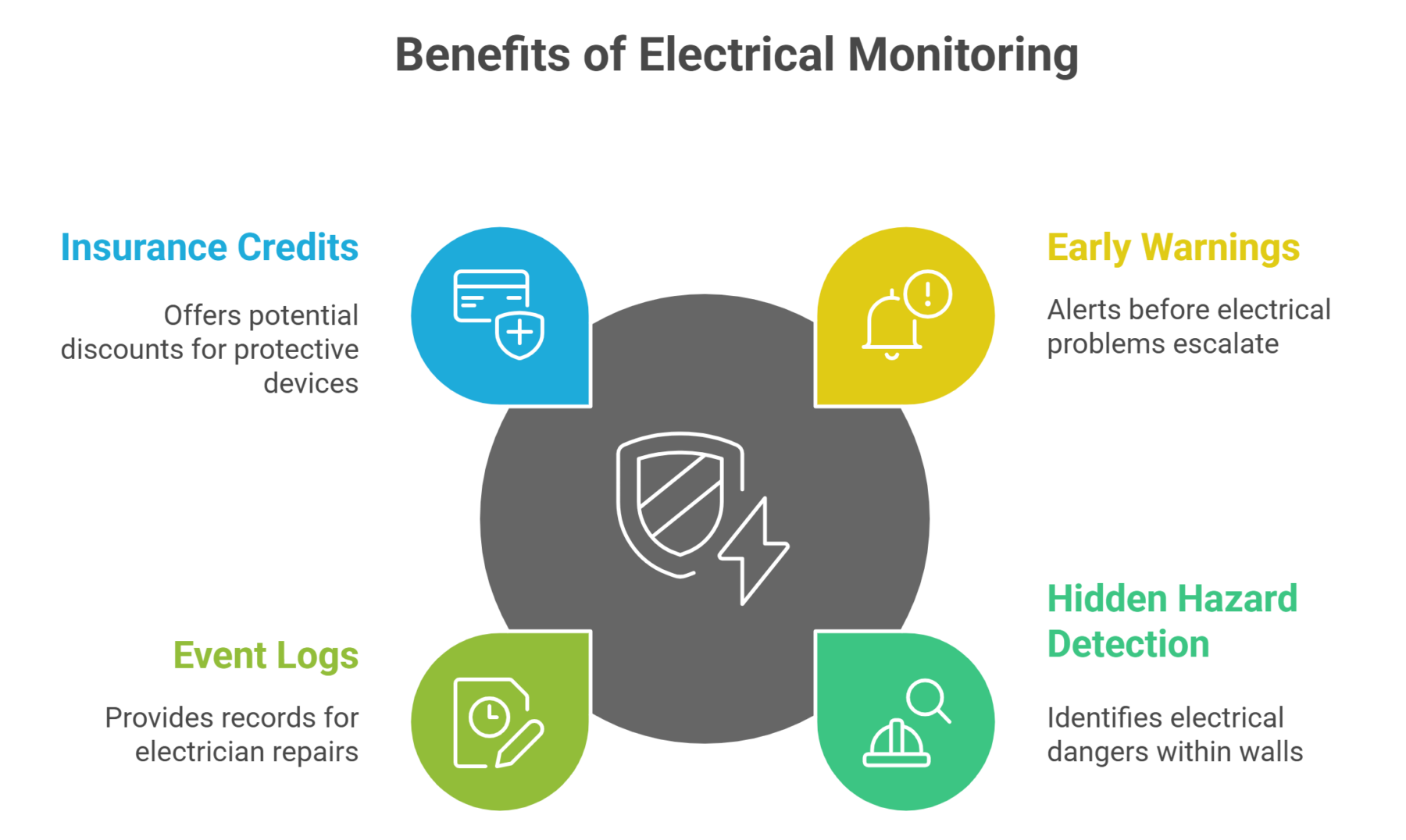

Consider getting an electrical monitoring device

Electrical fire risks increase during colder months because of space heaters and heavy holiday power use. A plug-in or whole-home electrical monitor can detect issues like arc faults, overheating, or loose neutrals inside your walls and send alerts through an app.

This gives you:

- Early warnings before a problem becomes dangerous

- Detection of hidden electrical hazards

- Clear event logs your electrician can use for repairs

- Possible credits for protective devices (where available)

For best results, install the device before peak winter usage, respond quickly to any alerts, and keep records of installation and repairs in case your insurance agent needs them.

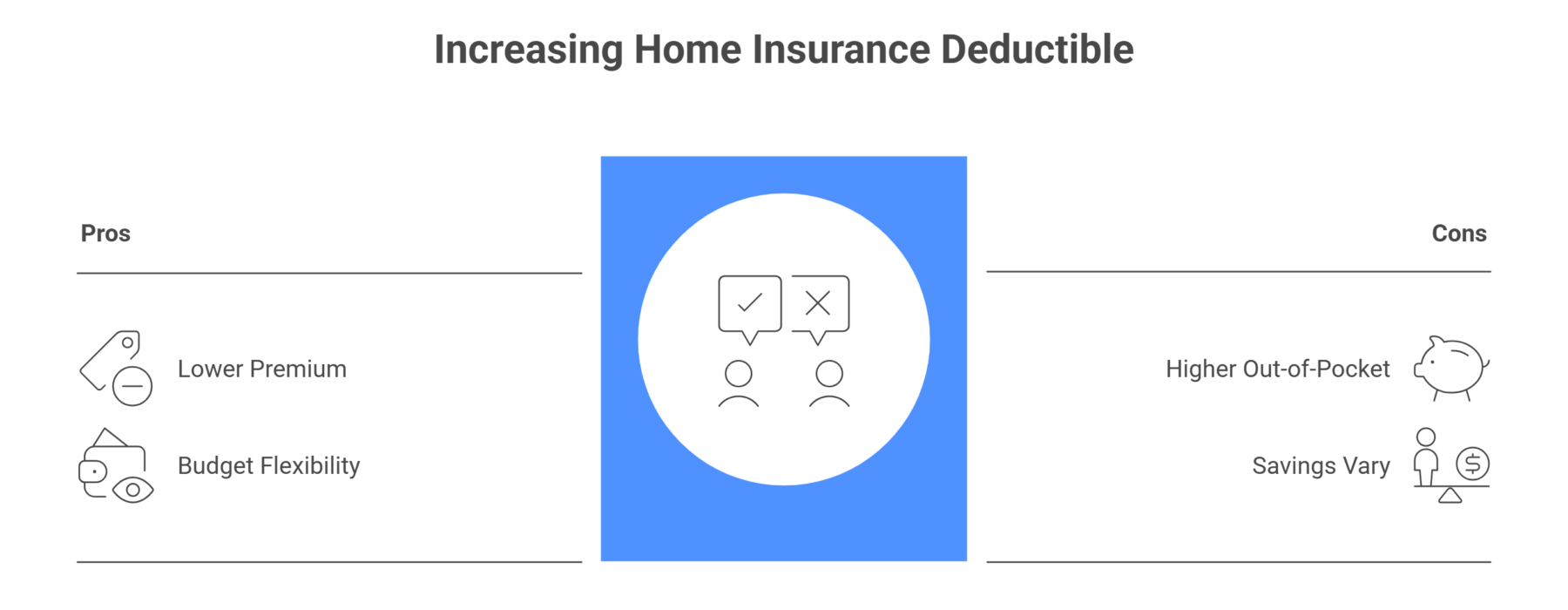

Review Your Deductible

If your budget allows, increasing your home insurance deductible from, say, $1,000 to $2,500 could lower your premium noticeably.

Just make sure it’s an amount you’d be comfortable covering if you ever need to file a claim and remember, savings vary by carrier, state, and loss history.

The Bottom Line

Energy efficiency alone doesn’t directly lower your insurance rate, but when your improvements also reduce the risk of fire, freezing, or water damage, it can help your future rating and insurability.

So before winter sets in, focus on upgrades that make your home safer, smarter, and better protected. You’ll likely see the payoff in fewer issues, smoother renewals, and maybe even some savings along the way.

At PNW Insurance, we’re here to help you make the most of your coverage and your home.

If you’re planning any upgrades before winter, talk to our team. We’ll help you understand how your changes could impact your policy and make sure your protection fits your home, your budget, and your season ahead.

While you’re at it, it’s a great time to review your current credits, including monitored alarm systems, automatic water shutoff devices, smart sensors, automatic backup generators, loss-free discounts, and deductible options.

Learn More From the PNW Team on YouTube

If you found this helpful, we share even more practical, real-life insurance guidance on our YouTube channel.

On our channel, you’ll find:

- Quick breakdowns of common insurance questions

- Home, auto, and business coverage tips

- Claim scenarios (what’s covered vs. what’s not)

- Ways to avoid costly mistakes and protect what matters most

Head over to our YouTube channel and subscribe to stay informed, prepared, and confident about your coverage.