A mortgage escrow account is generally meant to make life easier—automatically handling your homeowners insurance payments so you don’t have to think about them every year. For the most part, it works as intended. That said, there are situations where relying solely on escrow might create unexpected issues. Loan transfers, clerical slip-ups, or missed updates with your lender can sometimes lead to unpaid insurance premiums – or even a temporary lapse in coverage. That could leave your home at risk right when you need protection most. Let’s take a closer look at why this can happen and a few ways to help safeguard what’s likely your biggest investment.

How Escrow Accounts Work (and Where They Can Go Wrong)

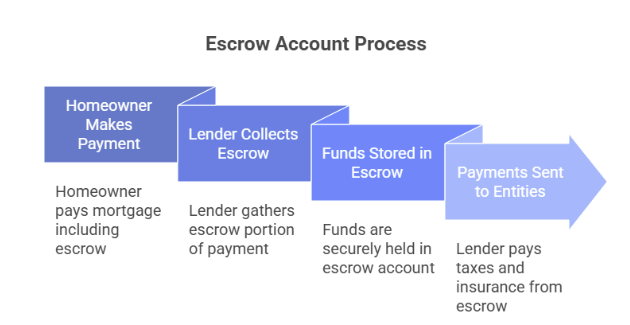

Mortgage escrow accounts are usually designed to simplify things. In most cases, your lender collects a portion of your insurance premium and property taxes with your monthly mortgage payment, then forwards those funds to pay the bills on your behalf.

A Few Scenarios Where Issues Might Pop Up

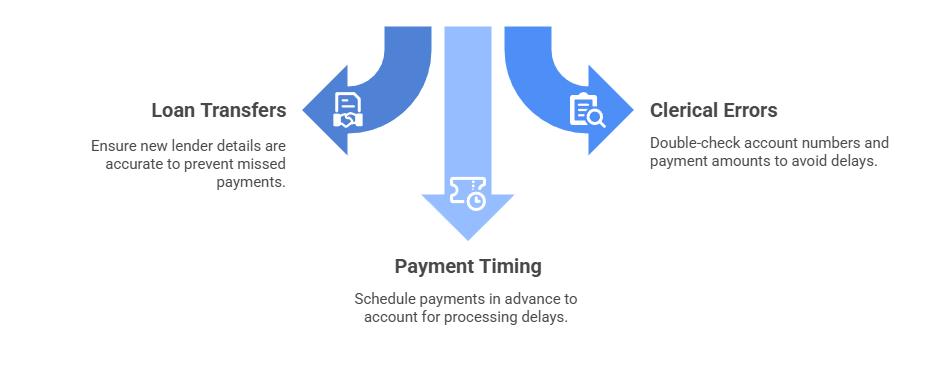

While things often run smoothly, there are situations where escrow payments don’t go exactly as planned. These aren’t everyday occurrences, but they do happen often enough that it’s worth being aware of them. Below are a few examples of where things can sometimes get off track.

- Loan Transfers: When your mortgage is sold to another lender, some details can get lost in the shuffle, potentially causing a missed payment.

- Clerical Errors: Small mistakes, like a wrong account number or payment amount, can delay or prevent a payment. There are several ways these kind of errors can happen.

- Payment Timing: Even if funds are available, delays in processing or scheduling can occasionally cause a payment to be late.

It’s important to stay alert if you ever receive a late payment notice on your home policy. Don’t assume your escrow has it covered—take a moment to verify. Reaching out to your insurance agent or lender right away can help ensure everything is handled correctly and your coverage stays uninterrupted.

What Can Happen if an Escrow Payment Gets Missed

If your lender notices a gap in coverage, they may purchase a policy on your behalf. These policies generally protect the lender’s interest more than yours and can be more expensive, with limited coverage for personal belongings or liability.

Other potential consequences include:

- Possible Loss of Coverage

If a policy lapses, there may be a period where your home isn’t protected against risks like fire, theft, or liability claims. Should a loss occur during that time, homeowners are often responsible for the costs themselves. - Credit and Financial Impacts

Some lenders may apply fees or penalties when coverage lapses. In certain cases, gaps in insurance history can also make refinancing or securing future loans a little more complicated. - Challenges with Reinstatement

If a lapse occurs, some insurers may see it as a higher risk. That can sometimes mean higher premiums or difficulty finding a replacement policy right away. - Potential Liability Concerns

In the event someone is injured on your property during a lapse, liability claims could become a significant out-of-pocket expense without insurance protection in place.

PNW Insurance Tips for Homeowners Relying on Escrow

Keep an Eye on Escrow Statements

It may be worth reviewing your escrow statements from time to time to confirm payments are being applied the way they should. Catching small discrepancies early can sometimes help prevent bigger issues later.

Stay in Touch with Your Insurance Carrier

If your mortgage servicer changes, giving your insurer a quick update can help reduce the chance of missed payments. It can also be a good idea to check in occasionally to confirm your premiums are being received on time.

Set Up Alerts

Many insurance carriers and lenders offer reminders for renewals or missed payments. Taking advantage of these alerts can provide an extra layer of peace of mind.

Keep a Small Safety Net

Having a little set aside for emergencies could help cover a premium if an escrow hiccup ever happens. It’s not always necessary, but it can be reassuring.

Understand Force-Placed Insurance

Force-placed insurance can come into play if a policy lapses. These policies tend to cost more and usually provide less coverage, which is why many homeowners try to avoid them when possible. The often only provide coverage for the bank in the event of a loss, not the homeowner.

Check Your Policy Annually

Taking time once a year to review your coverage limits and endorsements can help you make sure they still align with your needs and lifestyle

Learn More From Michelle Hancock on YouTube

Want to learn more? Michelle Hancock, Agency Owner and Co-Founder of PNW Insurance Group, shares a video on this very topic over on our YouTube channel. Watch the full video here.

While you’re there, you’ll also find other helpful discussions on insurance-related situations that might come up in everyday life. It’s a great way to stay informed and get practical tips all in one place.

Don’t Let Escrow Mistakes Put Your Home at Risk

Your escrow account can be a really useful tool, but like anything else, it’s not perfect. By staying a little proactive and keeping the lines of communication open with your lender and insurance carrier, you may be able to reduce the risk of missed premiums or lapses in coverage.

Talk to your insurance agent, or connect with us today to review your policy and explore strategies that can help safeguard your biggest investment.

If you’re in the Pacific Northwest, we proudly serve clients in Washington, Oregon, Idaho, Montana, and Arizona.

Because when it comes to protecting your home, it’s better to leave as little to chance as possible.