Historic Flooding Reached Unexpected Areas

In December 2025, parts of Washington State experienced historic flooding linked to a powerful series of atmospheric river events. While flooding is often associated with high-risk zones, reports suggested that some properties located in Flood Zone X, which is typically considered lower risk, were also impacted.

For many homeowners, this raised an important question: if an area is labeled “low risk,” how can flooding still occur?

Understanding what happened and what it may mean for homeowners can help provide useful context moving forward.

What Happened During the Washington Atmospheric River Event

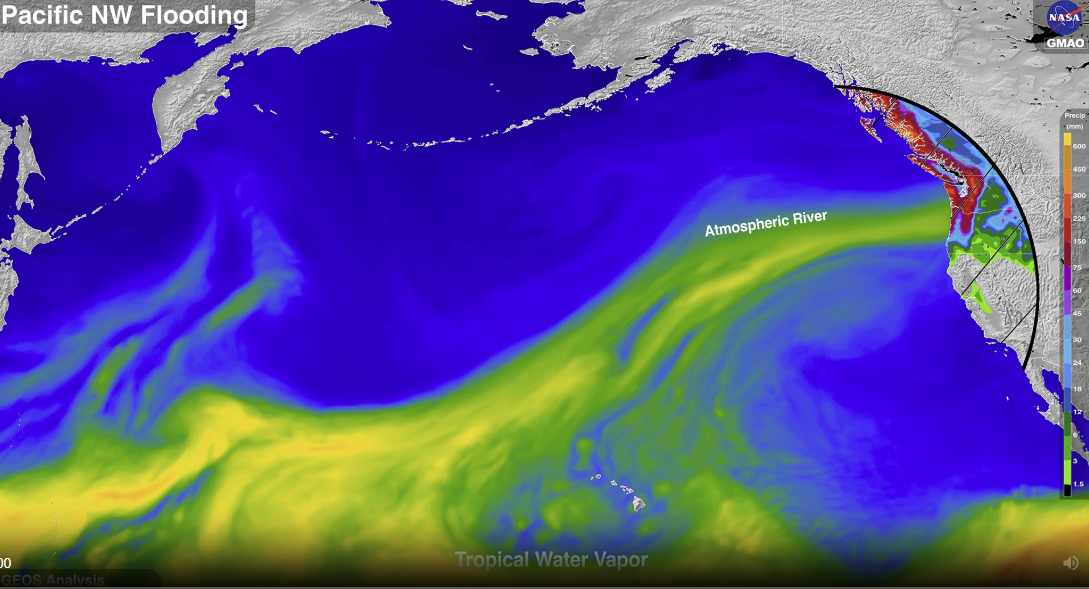

Image Courtesy of NASA’s Global Modeling and Assimilation Office and NASA’s Scientific Visualization Studio

An atmospheric river is essentially a long, narrow band of concentrated moisture in the atmosphere that carries large amounts of water vapor from tropical regions toward land. When it reaches mountains or cooler air, that moisture can fall as heavy rain or snow, sometimes delivering days’ worth or even weeks’ worth of precipitation in a short period.

Between December 5 and December 19, 2025, a strong and persistent high-pressure system developed over the southwest coast of the United States. This weather pattern helped direct multiple atmospheric rivers into the Pacific Northwest, bringing prolonged and intense rainfall.

In some areas, rainfall totals reportedly reached about a month’s worth of precipitation in just a few days. Several of Washington’s largest rivers approached or reached record levels, and dozens of additional rivers experienced flooding.

When rainfall occurs at this scale and duration, water systems and flood control infrastructure may become overwhelmed, allowing water to extend beyond typical floodplain boundaries

Image Courtesy of governor.wa.gov

.

What Is Flood Zone X and How Does It Compare to Other FEMA Flood Zones?

Graphic Courtesy of Putnam County Emergency Management

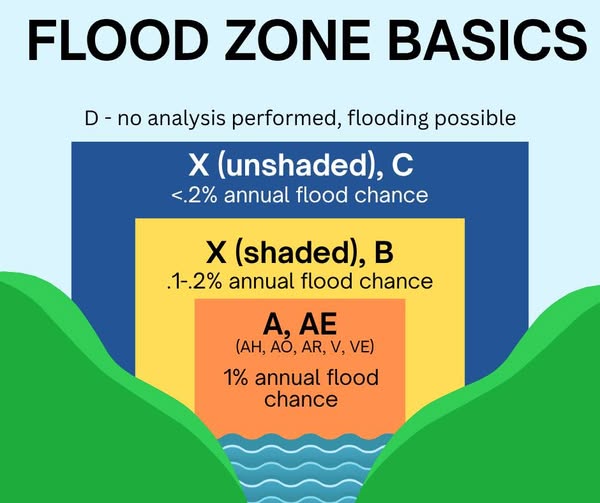

FEMA flood maps group areas based on estimated flood risk. These zones are based on historical data and models, so they indicate probability, not certainty.

- Zone D (Undetermined risk) are areas that have not undergone detailed flood risk analysis, so the level of risk is uncertain, though flooding may still be possible.

- High-risk zones (like A or AE) are part of the Special Flood Hazard Area (SFHA) and generally have a 1% annual flood chance. Lenders typically require flood insurance in these areas.

- Moderate-to-low risk zones, including Flood Zone X (shaded or unshaded), are usually outside the SFHA. Unshaded Zone X generally represents lower risk, often less than a 0.2% annual chance of flooding, while shaded Zone X indicates a slightly higher, moderate level of risk, typically between a 0.2% and 1% annual chance. Because the statistical risk is lower, flood insurance is generally not federally required by lenders.

- Areas without a listed flood zone – In some cases, a property may not have a specific flood zone designation. This generally suggests a lower likelihood of flooding based on available data, but it does not completely rule out the possibility.

However, “lower risk” doesn’t always mean “no risk,” since flooding can still happen due to heavy rain, drainage issues, or changing environmental conditions.

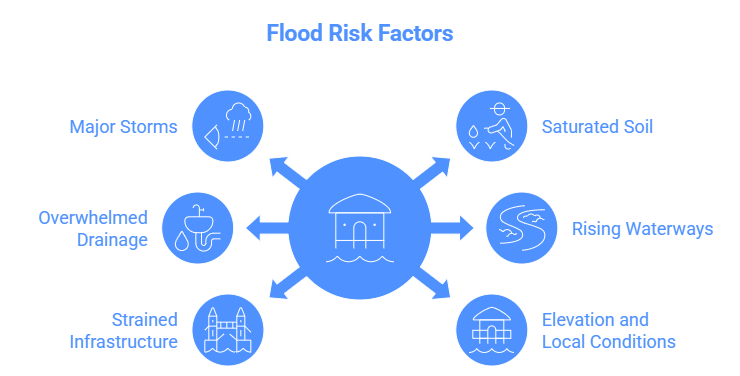

Why Some Lower-Risk Areas Still Experienced Flooding

- Major storms (like recent atmospheric river events) can bring rainfall that exceeds historical norms

- Saturated soil and overwhelmed drainage systems reduce water absorption

- Rivers and waterways may rise beyond mapped floodplain limits

- Local infrastructure can become strained during intense weather

- Flood risk depends on more than zone—elevation and local conditions matter

Water damage from flooding can be costly, especially when structural components or mold remediation are involved. Understanding how water events are categorized and what coverage applies helps homeowners plan ahead and make informed decisions.

An Option for Lower-Risk Areas: Preferred Risk Policies

For homes located in moderate-to-low risk areas such as many Zone X properties, the NFIP sometimes offers what is known as a Preferred Risk Policy (PRP).

These policies are designed for properties that historically have had lower expected flood risk, and they are often priced differently than policies for higher-risk zones.

Eligibility requirements and timing rules can vary, so homeowners may want to check whether their property qualifies.

Local Resources for Washington Homeowners

Homeowners who want to explore flood risk or preparedness resources may find helpful information through several Washington state agencies:

Washington Department of Ecology

Coordinates floodplain management and mapping programs across the state.

Washington Emergency Management Division

Provides disaster preparedness guidance and statewide emergency response information.

Washington Office of the Insurance Commissioner (OIC)

Offers consumer resources and assistance related to insurance questions, complaints, or claims.

For national flood map information, homeowners can also explore the FEMA Flood Map Service Center, where maps and property-level flood zone details are available.

PNW Insurance Tips Homeowners Might Consider

While situations vary, homeowners in the Pacific Northwest can take practical action steps now:

- Check flood risk: Use the Federal Emergency Management Agency Flood Map Service Center or speak with your agent to confirm your flood zone and panel.

- Review your policy: Look for flood exclusions and document property conditions with photos, videos, and elevation details.

- Get a flood insurance quote: Coverage often requires a 30-day waiting period before it takes effect, so planning ahead matters.

- Consider elevation documentation: An Elevation Certificate can help determine risk and potential insurance requirements if you’re near the Base Flood Elevation.

- Understand FEMA map tools (LOMA / LOMR): A Letter of Map Amendment or Letter of Map Revision may adjust how a property is classified on flood maps if certain criteria are met. These processes can be technical, so surveyors or professionals familiar with FEMA mapping often assist homeowners.

- Explore private flood insurance options (insurance tip): In addition to National Flood Insurance Program coverage, private flood policies may offer different benefits such as higher coverage limits or replacement-cost options. Terms, pricing, and underwriting vary by carrier, so comparing options can help you choose coverage that fits your needs.

- Ask questions early: Understanding how coverage works before a claim helps avoid surprises.

- Stay prepared: Keep property documentation and awareness of local emergency plans and seasonal risks.

- Seek professional guidance: A review of coverage can help identify gaps and solutions aligned with your needs and comfort level.

The Flood Coverage Gap Homeowners May Not Realize

One common misconception is that standard homeowners insurance includes flood damage. In many cases, flood-related losses are typically excluded under standard policies, regardless of whether a home is located in a high-risk or lower-risk zone.

Because flood insurance is often not federally required in Flood Zone X, some homeowners may choose not to carry it. Others may still explore federal or private flood insurance after reviewing what their existing policy does and does not cover.

It’s also worth noting that most new flood policies including those through the National Flood Insurance Program (NFIP), generally include a waiting period (often around 30 days) before coverage begins, with a few limited exceptions. Understanding both coverage limitations and timing can help homeowners make more informed decisions about their protection. Even if your lender doesn’t require it, we’d recommend considering all the data about where you live and making an informed choice about buying it.

Understanding NFIP Coverage Limits

Another point worth knowing is that NFIP flood policies have nationally standardized coverage limits.

These limits apply separately to:

- Building coverage (the structure itself)

- Contents coverage (personal belongings inside the home)

Because they are separate coverages, homeowners typically need to choose whether they want one, the other, or both.

Some homeowners discover that the standard limits may not fully match their home’s replacement value, which is one reason some people also explore private flood insurance options that may offer higher limits or additional features.

Reviewing both options can help homeowners understand what might best align with their situation.

Frequently Asked Questions About Flood Coverage (Practical FAQs)

Q: If I’m in Zone X, do I need flood insurance?

A: Lenders usually don’t require it, but flood risk isn’t zero. Homeowners should evaluate personal risk based on location, elevation, and past weather patterns.

Q: How long until coverage starts?

A: New flood policies often have a ~30-day waiting period. Verify specifics with your carrier.

Q: Will homeowners insurance pay for flooding?

A: Standard policies typically exclude flood damage. Coverage for water may apply in limited situations (e.g., wind-driven rain or plumbing issues), but surface flooding is usually excluded.

Learn More From the PNW Team on YouTube

Insurance topics can sometimes feel overwhelming, especially when coverage details and risk factors vary from situation to situation. That’s why the PNW team regularly shares helpful, easy-to-understand videos on our YouTube channel covering common questions, practical insurance tips, and real-world scenarios homeowners and business owners may face. Our goal is simply to help you feel more informed so you can make decisions with greater confidence.

And of course, if something raises questions about your own policy or situation, you can always reach out to the PNW team. We’re happy to help review your coverage, walk through possible options, and guide you through the process whenever you need support. Contact us here!

Additional Context on Lender Requirements

Mortgage lenders typically follow FEMA flood maps when determining insurance requirements.

Properties located within Special Flood Hazard Areas (SFHA), such as Zones A or AE, generally require flood insurance as a condition of federally regulated mortgages.

Homes outside those areas, including many Zone X properties, are usually not federally required to carry flood insurance, though homeowners may still choose to explore coverage voluntarily depending on their comfort level with risk.

Compliance Note

Educational Disclaimer

This article is intended for general educational purposes only and does not represent a coverage determination.

Insurance coverage depends on the specific policy language, endorsements, and underwriting conditions involved. Homeowners should review their individual policy documents and consult their insurance professional for guidance related to their specific situation.

Last Updated: March 2026

Flood maps, insurance programs, and policy details can change over time. Readers are encouraged to verify the most current information through FEMA and relevant state agencies.