When most people think about homeowners insurance, they picture coverage for fire, theft, or natural disasters. But there’s a critical piece that often gets overlooked: home liability insurance.

This protection can mean the difference between financial security and devastating loss if an accident happens on your property or even away from home.

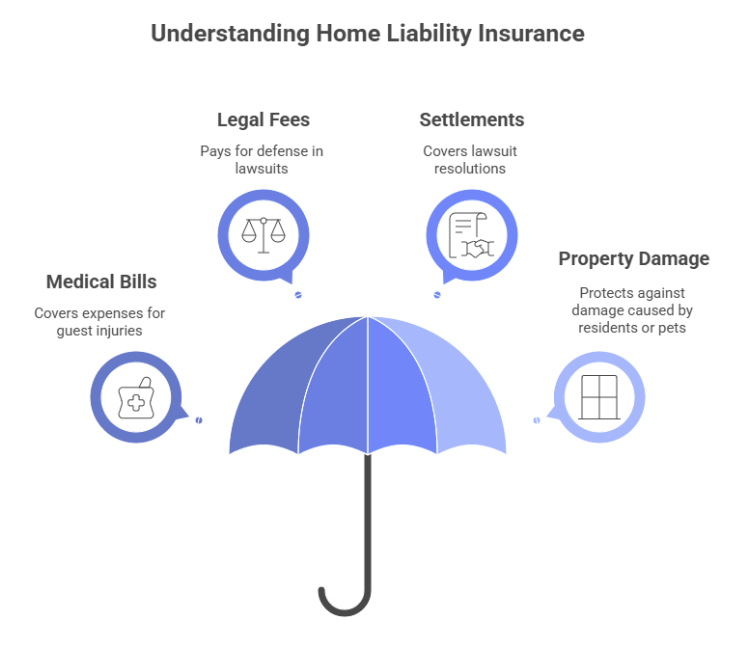

What Is Home Liability Insurance?

Home liability insurance protects you financially if you’re found legally responsible for injuries or property damage to others. It typically covers:

- Medical bills for injuries sustained by guests on your property.

- Legal fees if you’re sued.

- Settlements or judgments resulting from lawsuits.

- Property damage caused by you, your family, or even your pets.

And here’s the part many people don’t realize: liability coverage may apply to more than just incidents at your home. It can also cover accidents that happen away from your property, like if your dog knocks someone over at the park or you accidentally damage someone’s belongings while traveling.

Scenarios Where Liability Insurance Applies

Here are a few examples that help illustrate the kinds of situations where liability coverage can be especially valuable:

Dog-Related Incidents

Even the calmest dogs can have an off day. Say your usually well-behaved dog gets excited when a guest arrives and jumps on them, leading to a fall and a wrist injury. Depending on the severity, medical bills for surgery or therapy could reach tens of thousands of dollars. If the guest also decided to pursue legal action for things like lost wages or pain and suffering, the overall costs could climb significantly. In situations like this, liability insurance may help cover those expenses and ease the financial burden. We covered this topic on our YouTube channel, check it out here.

Accidents Away from Home

Liability coverage doesn’t always stop at your front door. For instance, if you’re visiting a friend’s home and accidentally break an expensive antique, you might otherwise be responsible for replacing it out of pocket. With the right coverage in place, your policy could help handle those costs, potentially saving you from a stressful and costly situation.

Unintentional Injuries

Household mishaps happen more often than we’d like to admit. Imagine a guest tripping on a loose rug in your living room and suffering a broken wrist. Beyond medical expenses, there’s always the chance they could claim negligence and pursue legal action. Legal fees alone can add up quickly, and settlements can push the total higher. Liability insurance can provide a layer of protection so that one accident doesn’t spiral into a major financial setback.

Libel and Slander

With so much of our lives playing out online, even casual social media posts can sometimes create issues. If a comment or review unintentionally harms someone’s reputation, they may decide to sue for defamation. Legal defense costs and potential damages in these cases can be surprisingly high sometimes well into six figures. Many policies include coverage for this or it can be added and that might help provide peace of mind. We covered this topic on our YouTube channel, check it out here.

What Are Standard Liability Limits on Home and Umbrella Policies?

Most home insurance policies in the U.S. come with liability coverage, but the limits can vary. Here’s a general idea of what you might see:

- Standard Liability Limits: Many policies include a starting limit of around $100,000.

- Higher Limits Available: It’s often possible to bump this up to $300,000 or $500,000, sometimes for only a modest increase in your premium.

- Umbrella Policies: For those who want broader protection, umbrella policies can add extra coverage usually starting at $1 million and extend over both home and auto insurance.

Is $100,000 Liability Coverage Enough?

Plenty of homeowners stick with the default $100,000 liability limit, assuming it’s enough. But whether it truly covers your risks depends on your lifestyle, assets, and exposure to potential claims. Let’s look at why $100,000 might come up short and when it could still work as a basic safety net.

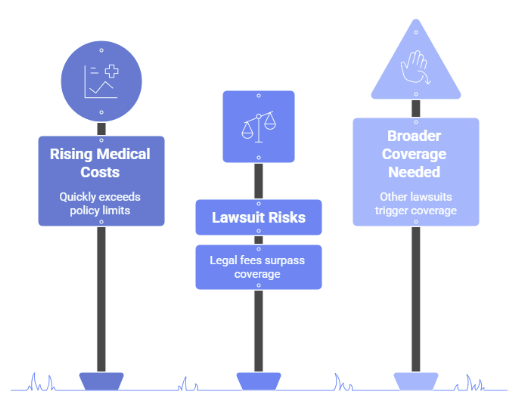

Why $100,000 May Be Insufficient

- Rising Medical and Legal Costs

Serious injuries or lawsuits can quickly exceed $100,000. Hospital stays, surgeries, and rehab expenses add up fast, and anything beyond your policy limit could fall on you personally. - Lawsuit Risks

Slip-and-fall claims, dog bites, or even an accident you’re found responsible for could lead to settlements and legal fees that stretch well past $100,000. Your personal savings, investments, or even your home could be at risk. - Broader Coverage Needs

Liability isn’t just about physical injuries. Property damage, libel, or slander cases can also trigger claims, and $100,000 may not go very far in these scenarios.

How Much Liability Coverage Do You Need?

There’s no one-size-fits-all answer here, the “right” amount of liability coverage really comes down to your personal situation. A good starting point is to look at your assets, lifestyle, and exposure to potential risks. Please keep in mind, there is no number here that is the “right” amount, it is simply doing the best you can with the resources you have to protect yourself. Here are a few things to keep in mind:

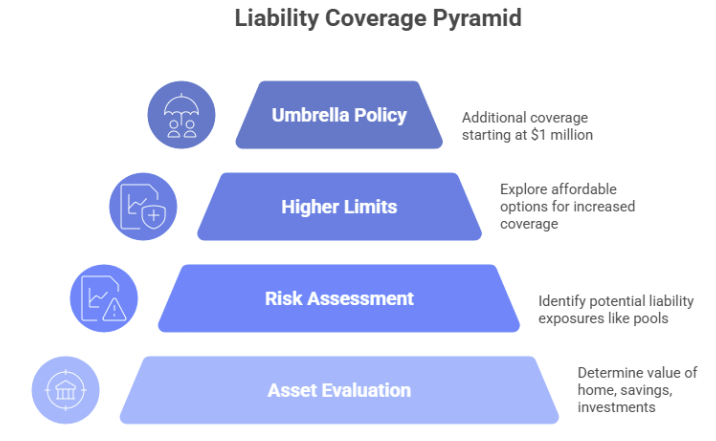

- Evaluate Your Assets: It’s generally wise for your liability limit to cover the value of your home, savings, and other assets. That way, if a large claim ever came your way, you’d have a stronger financial safety net. It is at least, a great place to start!

- Consider Your Risks: Certain factors like having a pool, trampoline, frequent visitors, or even pets can increase your chances of facing a liability claim.

- Get Quotes for Higher Limits: Moving from $100,000 to $300,000 or $500,000 is often more affordable than people realize, and it can add a lot of extra peace of mind.

- Add an Umbrella Policy: If you’re looking for broader protection, an umbrella policy could be worth considering. These typically start at $1 million in coverage and extend over both your home and auto policies.

Unsure about the right amount of coverage? An insurance agent can help you sort through your options and find the right fit for your situation.

The Cost of Increasing Your Coverage

A lot of people are surprised to learn that boosting liability coverage doesn’t always mean a big jump in cost. In many cases, it can be relatively affordable:

- Higher Home Policy Limits: Raising a standard liability limit from $100,000 to $500,000 might only add somewhere in the ballpark of $20–$50 per year, depending on the insurer and your situation.

- Umbrella Policies: Adding an umbrella policy often starting at $1 million in coverage can sometimes cost around $150–$300 annually.

For many households, those extra dollars can translate into a much stronger safety net.

Common Exclusions to Watch Out For

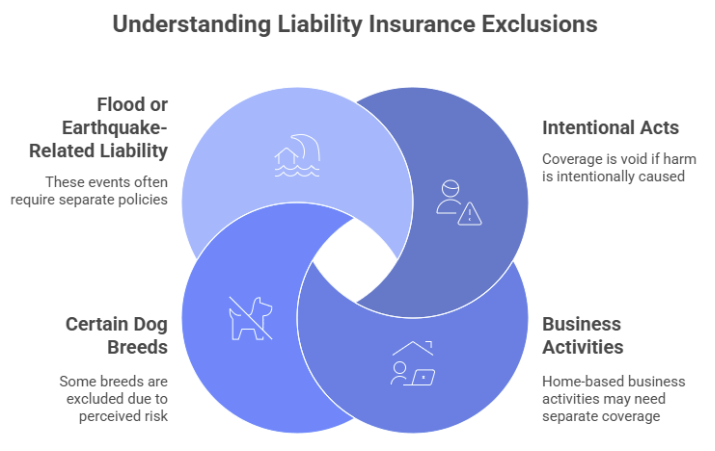

While liability insurance can cover a wide range of situations, there are still some areas where it usually won’t apply. Depending on your insurer and policy, exclusions might include things like:

- Intentional Acts: Coverage generally doesn’t apply if harm or damage is caused on purpose.

- Business Activities: Claims related to a home-based business often require separate business liability coverage.

- Certain Dog Breeds: Some insurers may exclude specific breeds they consider higher risk.

- Flood or Earthquake Liability: These types of events often call for separate policies or endorsements.

Because exclusions can vary, it’s always a good idea to review the fine print of your policy and ask your agent about any gray areas that might affect your coverage.

Pro Tips for Maximizing Your Liability Protection

Here are a few ways you might strengthen your liability coverage:

- Review Your Policy Regularly: Your coverage may need to adjust as your assets, lifestyle, or risks change.

- Ask About Endorsements: Depending on your situation, endorsements for things like a home-based business or high-value items could be worth exploring.

- Bundle Policies: Bundling home and auto insurance can sometimes make it more affordable to add an umbrella policy.

- Understand Your Deductible: While liability claims usually don’t involve a deductible, property damage claims connected to them sometimes do.

From unexpected dog-related incidents to potential lawsuits, the right coverage can go a long way in helping protect you from life’s curveballs. It’s often worth taking time to review your policy, consider higher limits, or look into umbrella coverage if it fits your needs.

Want to dive deeper? We’ve covered this topic on our YouTube channel, sharing real-life stories, expert insights, and practical tips. And if you’re unsure where to start, your insurance agent can walk you through your options and help you find coverage that makes sense for your situation.

Learn More From Michelle Hancock on YouTube

Michelle Hancock, Agency Owner and Co-Founder of PNW Insurance Group, has been an insurance agent for many years. Over those years, she has seen firsthand, and heard countless stories about how quickly accidents can spiral into costly liability claims.

On our YouTube channel, she shares a real-life example that underscores just how unpredictable and financially devastating these situations can be.

It’s a must-watch for anyone looking to better understand the importance of being prepared. After all, accidents don’t send a warning, they just happen. The best way to protect yourself, your family, and your assets is by ensuring you have the right liability coverage in place. Check out the video and take the first step toward peace of mind today.