When people think about homeowners insurance, the first thing that comes to mind is the house itself—protecting the walls, the roof, and everything inside. But what about the detached garage, shed, or treehouse in your backyard? That’s where Coverage B (Other Structures) comes in.

If you’re a homeowner (or just curious about how insurance works), knowing how this part of your policy works can save you from some expensive surprises. We’ve provided some general details and information below, but as always, it’s important to research with your agent on your policy.

What Are Other Structures?

In insurance terms, “other structures” refer to buildings or structures on your property that are separate from your main residence. To qualify, these structures must meet specific criteria:

- Detached from the Dwelling: The structure must be physically separate from your home. If it’s connected by something minor, like a utility line or fence, it still qualifies.

Examples: Garages, Sheds, Barns, Pole Buildings and Gazebos, would be just a few examples of unattached structures.

Essentially, if it’s not attached to your house and serves a purpose other than being part of the main dwelling, it likely falls under this category.

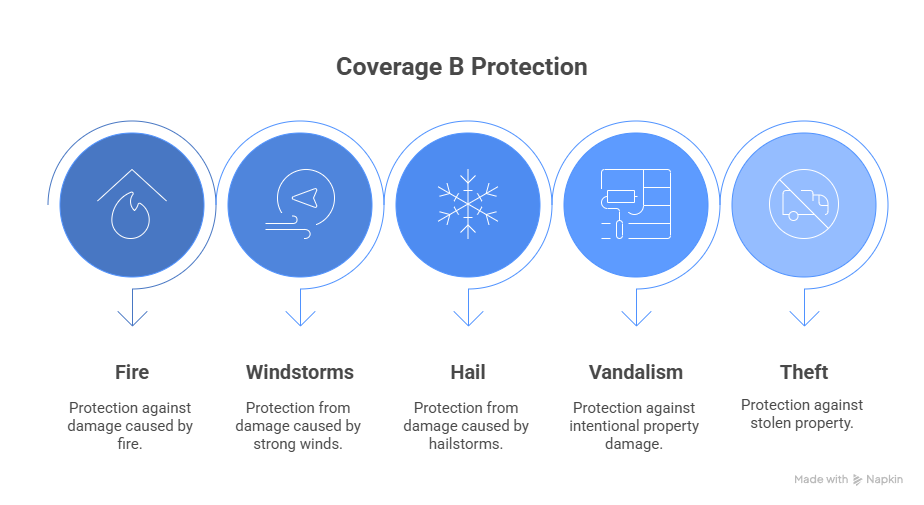

What Does Coverage B (Other Structures) Protect?

Coverage B (Other Structures) is designed to protect these structures from the same perils covered under your main dwelling policy. This typically includes:

For example, if a tree falls on your detached garage during a storm, Coverage B (Other Structures) would help pay for the repairs.

What’s Not Covered?

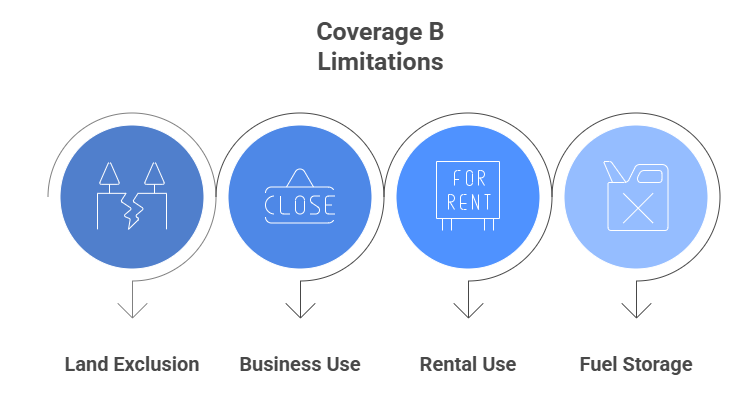

While Coverage B (Other Structures) offers valuable protection, it does have limitations:

- Land Exclusion: The land beneath the structure isn’t covered. If the ground shifts or erodes, you’re out of luck.

- Business Use: Structures used for business purposes are generally excluded. For instance, if you’re running a workshop out of your detached garage, it won’t be covered unless you add a specific endorsement.

- Rental Use: If you rent out a structure to someone who isn’t a tenant of your main home, it’s excluded—unless it’s used solely as a private garage.

- Fuel Storage: Storing fuel (other than what’s in a vehicle’s tank) disqualifies the structure from coverage.

How Much Coverage Do You Get?

The standard limit for Coverage B (Other Structures) is typically 10% of your Coverage A (Dwelling) limit.

For example, if your home is insured for $300,000, you’d have $30,000 in coverage for other structures. This is an additional amount of insurance, meaning it doesn’t reduce your dwelling coverage.

However, if you have high-value structures, you may need to increase this limit. A custom-built gazebo or a large pole barn could easily exceed the standard coverage amount.

Why Coverage B (Other Structures) Matters

Michelle Hancock, Agency Owner & Co-Founder of PNW Insurance Group, shared a story about her nephew (not a PNW client at the time) whose 30×60 shop was destroyed when a tree fell during a windstorm. He assumed it was covered, but since it wasn’t properly listed or valued under Other Structures, he had to pay a large portion of it out of pocket.

The lesson for you: always update your agent when you add or upgrade sheds, shops, or other detached buildings. A quick call can be the difference between full coverage and a costly surprise.

Watch Michelle share the full story in this video here.

When Should You Consider Additional Coverage for Other Structures?

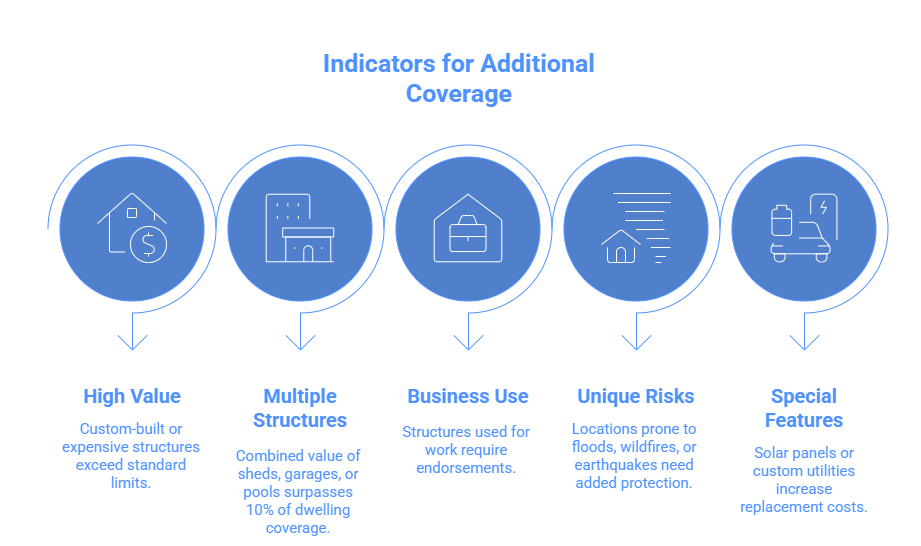

Most standard homeowners policies typically include 10% of your dwelling coverage for other structures, but that may not always be enough. Here are key indicators that you may need additional coverage for other structures.

- High Value: Custom-built or expensive structures exceed standard limits.

- Multiple Structures: Combined value of sheds, garages, or pools surpasses 10% of dwelling coverage.

- Business Use: Structures used for work require endorsements.

- Unique Risks: Locations prone to floods, wildfires, or earthquakes need added protection.

- Special Features: Solar panels or custom utilities increase replacement costs.

The Bottom Line

Coverage B (Other Structures) is an often-overlooked part of homeowners insurance, but it plays a crucial role in protecting your property. From detached garages to treehouses, this coverage ensures that the structures you’ve invested in are safeguarded against life’s unexpected events.

Take a moment to review your policy. Are your other structures adequately covered? If not, it might be time to talk to your insurance agent about increasing your limits or adding endorsements.

- Don’t forget to document your structures with photos and receipts. This makes the claims process smoother and ensures you’re reimbursed accurately.

- Regularly review your policy to ensure your coverage limits reflect the current value of your structures. Inflation and upgrades can leave you underinsured if not updated.

- Schedule an annual insurance check-up with your agent to discuss any changes to your property or potential risks.

We proudly serve clients in Washington, Oregon, Idaho, Montana, and Arizona. If you live in one of these states, reach out to us and we’ll help make sure every corner of your property is covered.

Talk to your insurance agent or connect with us today to see how Coverage B (Other Structures) can safeguard the spaces outside your main home