Rates are going up…. and insurance might become harder to even get! Yup, wanted to rip that band aid off right out of the gate as they say. Now, Let’s talk about it…..

There are certainly a lot of factors that go into rates. Some within your control and some a sign of the times, and ever changing inflation costs. This might help how you feel about rate increases, an insurance company must file statistical data to support an increase with the Office of the Insurance Commissioner and be approved any time they want to increase rates.

So what are the factors? Past loss history, credit score (yes it’s back in for most carriers in Washington), which city/area you live, driving history on auto, age of the home, age of the drivers, truly the list goes on and on.

Insurance carriers are required to remain solvent, meaning the amount of money they have access to is closely monitored. All these large storms, wildfires, costs of everything increasing, severity of accidents, etc etc etc impact every part of the insurance marketplace dramatically.

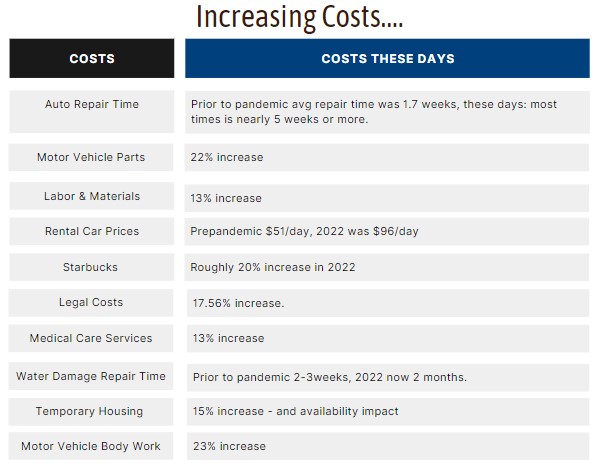

Since 2020 so much has changed, as we all know, but let’s narrow it down to how it impacts insurance. We can start with increase costs to repair and timeline to repair. If you have a loss in which you are displaced from your home, the cost for an insurance company to put you in alternative housing while yours is repaired has gone up roughly 15%. At the same time that cost jumped, so did the length of time you need to be in that temporary housing. Contractors and supplies are much harder to find and schedule and that isn’t easing up. Same is true on auto accidents, cost of vehicles, repairs, length of time, well you can well imagine how all of those things are a huge impact. Everything is taking longer, supply chain issues, labor issues, and we all know taking longer also means it costs substantially more.

That all seems quite depressing and might leave you wondering what you can do about it.

Talk to us! Be mindful that sometimes the best answer is stay where you are! Jumping around to a different insurance company can also impact your rates. If the rate is manageable, stay put, even if someone else is a a little cheaper today, it’s likely to change. That being said, sometimes the increase is too much to take, if that happens we can look to our fantastic line up of companies and see which one is a good fit for your situation. We can also review discount opportunities and make sure you are getting all you can.

Think about loss prevention. Earlier I said it might get harder to get insurance, what I meant by that is if you have a loss(es) on your insurance record, it might make things much more difficult for you. Of course, that is what you buy insurance for, but it was really intended for financially catastrophic loss. A loss that you cannot financially manage, or perhaps injury or overarching factors are present.

Do what you can to control, prevent or lessen the chances of a loss;

Keep up roof and exterior maintenance on your home

If the weather is dangerous outside – for many reasons, reconsider that trip to the store, etc

Cold snap coming? Make sure your house is prepared

Invest in home monitoring devices for water detection and a variety of other features. (This is a huge one, impacting all of our home rates here in the NW, these devices can help prevent water loss, one of the leading causes of loss in our area)

Did a small portion of a fence blow over? Might not want to turn that one in and “save” insurance for bigger events.

Discounts can be easy to get – bundle home and auto insurance (ask us how), consider a monitored alarm system in addition to smart home (discounts may exist for both)

Are you a safe driver – if so ask us about discounts based on your style of driving.

To wrap this all up, there are things you can do and it starts with knowledge. We wanted to provide you some “insider” information on the rating so we can help you from there. Our own personal policies are going up too, so we understand for sure! Please call us to learn more and talk about options.

Here is a graph, with information gathered from a variety of online sources about some expense changes in last couple years.

Thanks for reading and as always please feel free to call or text 253-527-6261 or email clientcare@pnwinsurancegroup.com